Fundraising for Startups: The Complete Guide to Raising Capital in 2026

Everything founders need to know about startup fundraising. Funding stages from pre-seed to Series C, how to build a data room, create a pitch deck, find investors, and close rounds.

TL;DR: Everything founders need to know about startup fundraising. Funding stages from pre-seed to Series C, how to build a data room, create a pitch deck, find investors, and close rounds.

Introduction

Fundraising for startups is the single biggest time sink a founder will face. The average Series A takes six months from first meeting to money in the bank. Some take longer. During those months, your product roadmap stalls, your team gets anxious, and your runway shrinks with every passing week.

I have been on both sides of this table -- raising capital for my own companies and advising founders through dozens of rounds. The pattern is almost always the same: founders who run a disciplined, structured fundraising process close faster and on better terms. Founders who wing it burn months, take bad deals, or fail to close at all.

This guide is the playbook I wish I had when I raised my first round. It covers every startup funding stage from pre-seed through Series C, walks through a step-by-step startup fundraising strategy, and gives you the frameworks, metrics, and tactical advice you need to cut your fundraising timeline in half.

Whether you are raising your first $500K or your fifth $50M, the fundamentals are the same. Let us get into it.

Startup Funding Stages Explained

Understanding startup funding stages is the first step to building the right fundraising strategy. Each stage has different expectations, different investors, and different benchmarks. Here is what you need to know about each one.

Pre-Seed ($50K - $500K)

Typical valuation: $1M - $5M

Timeline: 1 - 3 months

Who invests: Friends and family, angel investors, pre-seed funds, accelerators

At pre-seed, you are selling a vision. You might have a prototype or early MVP, but you probably do not have meaningful revenue. Investors at this stage are betting on the team, the market, and the problem you are solving.

What investors expect:

- A compelling founding team with relevant domain expertise

- A clear problem statement backed by personal experience or research

- An early prototype, wireframes, or evidence of demand (waitlist, LOIs)

- A large addressable market (TAM of at least $1B)

Key metrics: Team background, market size, early signal (waitlist signups, pilot conversations, LOIs from potential customers).

Seed ($500K - $3M)

Typical valuation: $5M - $15M

Timeline: 2 - 4 months

Who invests: Seed-stage VCs, angel syndicates, micro-funds

Seed is where you prove that people actually want what you are building. You should have an MVP in market, early customers or users, and initial signs of traction.

What investors expect:

- A working product with real users

- Evidence of product-market fit (retention, engagement, NPS)

- Early revenue or strong usage metrics

- A clear go-to-market hypothesis

- A team that can execute

Key metrics: MRR ($10K - $50K typical), user growth rate (15-20% month-over-month), retention curves, CAC, early unit economics.

Series A ($5M - $20M)

Typical valuation: $20M - $80M

Timeline: 3 - 6 months

Who invests: Series A VCs (Sequoia, a16z, Benchmark, Accel, etc.), multi-stage funds

Series A is the "prove you can scale" round. You have found product-market fit. Now investors want to see that you have a repeatable, scalable business model.

What investors expect:

- Clear product-market fit with strong retention

- A proven go-to-market motion (inbound, outbound, product-led, or channel)

- $1M+ ARR with consistent growth

- Efficient unit economics (LTV/CAC ratio of 3:1 or better)

- A plan to use the capital to accelerate growth

Key metrics: ARR ($1M - $5M), growth rate (2-3x year-over-year), net revenue retention (over 100%), gross margins (over 60% for SaaS), burn multiple (under 2x).

Series B ($15M - $50M)

Typical valuation: $80M - $300M

Timeline: 3 - 6 months

Who invests: Growth-stage VCs, crossover funds, late-stage specialists

Series B is about scaling what works. You have a repeatable playbook. Now you need capital to expand into new markets, hire aggressively, and build out your leadership team.

What investors expect:

- $5M+ ARR with strong growth trajectory

- Proven unit economics at scale

- A clear path to market leadership

- Experienced management team (VP-level hires in place)

- Multiple growth vectors (new products, new segments, international expansion)

Key metrics: ARR ($5M - $20M), growth rate (2x+ year-over-year), net revenue retention (over 110%), sales efficiency (over 0.7x), logo churn (under 10% annually).

Series C and Beyond ($50M+)

Typical valuation: $300M - $1B+

Timeline: 3 - 9 months

Who invests: Late-stage VCs, growth equity firms, PE firms, sovereign wealth funds, corporate VCs

At Series C and beyond, you are a proven business approaching an inflection point -- whether that is an IPO, a major market expansion, or a strategic acquisition. The due diligence is significantly more rigorous.

What investors expect:

- $20M+ ARR with a clear path to $100M

- Market leadership in at least one segment

- Strong unit economics and improving margins

- A credible path to profitability (or already profitable)

- World-class executive team

Key metrics: ARR ($20M+), revenue growth (50%+ year-over-year), Rule of 40 compliance (growth rate + profit margin over 40%), free cash flow trajectory, competitive moat.

When to Raise: Three Signals That the Timing Is Right

Timing your fundraise is as important as the raise itself. Go too early and you will either fail to close or take a bad deal. Go too late and you will be negotiating from a position of weakness.

Look for these three signals:

1. Product-Market Fit Indicators

You have product-market fit when customers are pulling the product out of your hands. The signs are unmistakable:

- Retention flattens: Your cohort curves level off instead of dropping to zero. Users stick around.

- Organic growth accelerates: Word of mouth becomes a real acquisition channel. Your NPS is above 40.

- Sales cycles shorten: Prospects move faster because the pain is acute and your solution is obvious.

- Expansion revenue grows: Existing customers buy more without heavy sales effort.

2. Runway Threshold

The rule of thumb: start raising when you have 9-12 months of runway left. This gives you enough time to run a proper process (3-6 months) without the desperation that comes from having 2 months of cash left.

If you wait until you have 3 months of runway, every investor will sense the urgency. Your negotiating leverage evaporates.

3. Growth Inflection

The best time to raise is when you can point to an inflection in your growth curve. Maybe you just crossed $1M ARR. Maybe your month-over-month growth jumped from 10% to 20% after launching a new channel. Maybe you just signed your first enterprise deal.

Investors want to fund acceleration, not survival. If you can show that more capital will directly translate into faster growth, you are in a strong position.

How Much to Raise: The 18-Month Rule

Raise enough to fund 18-24 months of operations and hit the milestones required for your next round. Here is the framework:

Step 1: Define your next milestone. For a seed-stage company, that might be $1M ARR. For a Series A company, it might be $5M ARR with proven unit economics.

Step 2: Build a bottoms-up budget. What does it cost to hit that milestone? Factor in headcount, marketing spend, infrastructure, and a buffer for things that take longer than expected (they always do).

Step 3: Add a buffer. Take your budget and add 20-30%. Fundraising takes longer than you think. Markets can turn. Key hires can fall through.

Step 4: Check the dilution math. Most rounds involve selling 15-25% of the company. If your budget says you need $3M and investors want 20%, your pre-money valuation needs to be $12M. Does that make sense given your stage and traction?

The dilution trap

There is a real tension between raising enough and raising too much. Over-raise and you dilute yourself unnecessarily, set expectations you cannot meet, and risk a down round later. Under-raise and you run out of cash before hitting your milestones, forcing you into a desperate bridge round.

The sweet spot: raise what you need for 18 months, plus a buffer, at a valuation that gives you a realistic shot at an up round next time.

Startup Fundraising Strategy: Step by Step

Here is the 10-step process I recommend to every founder. This is how you raise funding for a startup efficiently, without burning six months and your sanity.

Step 1: Define Your Fundraising Target and Timeline

Before you talk to a single investor, get crystal clear on:

- How much you are raising (use the 18-month framework above)

- Your target valuation range (research comparable deals at your stage)

- Your timeline (aim for 8-12 weeks from first meeting to close)

- Your minimum viable round (the smallest amount that still lets you hit your milestones)

Write these numbers down. Share them with your co-founders and advisors. When you are in the middle of fundraising and emotions are running high, these anchors will keep you grounded.

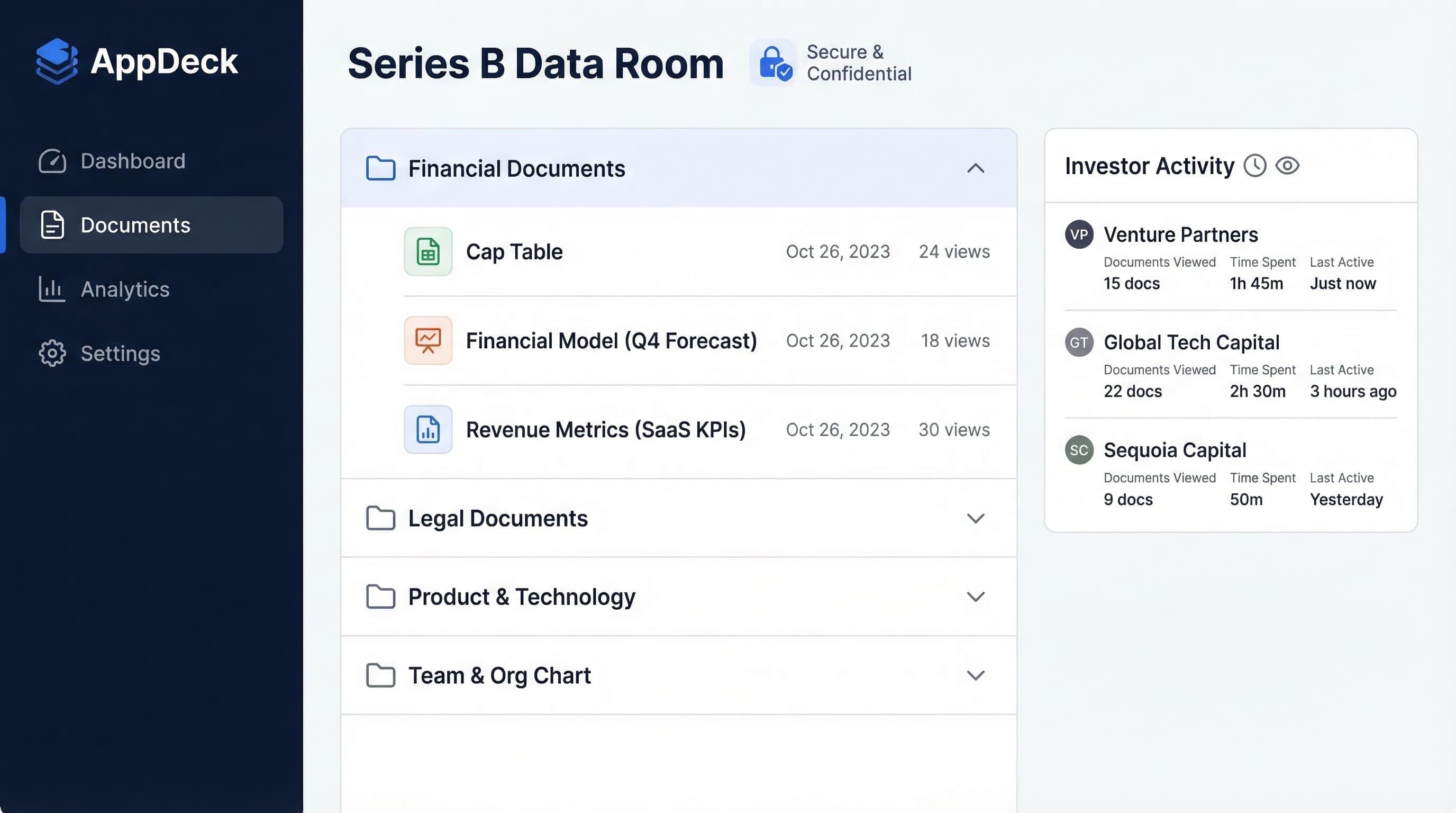

Step 2: Build Your Investor Data Room

Your data room is the single most important asset in your fundraising process. A well-organized data room signals that you are a serious operator. A missing or sloppy data room signals the opposite.

Set up your investor data room 4-6 weeks before you start taking meetings. This is not something you want to scramble on while investors are waiting.

What to include:

- Company overview and executive summary

- Pitch deck (current version)

- Financial model with historical actuals and projections

- Cap table

- Key contracts and customer agreements

- Team bios and org chart

- Product roadmap

- IP documentation

- Corporate documents (certificate of incorporation, bylaws, board resolutions)

I go deep on data room structure and security in my investor data room best practices guide. If you are setting up a data room for the first time, start there.

For a complete list of everything investors will request during diligence, see our due diligence checklist.

Step 3: Create Your Pitch Deck

Your deck is your calling card. It gets you in the door. Keep it to 12-15 slides:

- Title slide -- Company name, one-line description, your name

- Problem -- The pain point, who feels it, why existing solutions fall short

- Solution -- What you built and how it solves the problem

- Demo/Product -- Screenshots or a brief walkthrough

- Traction -- Your best metrics (revenue, growth, retention, logos)

- Market -- TAM/SAM/SOM with bottoms-up analysis

- Business model -- How you make money, pricing, unit economics

- Go-to-market -- How you acquire and retain customers

- Competition -- Your differentiated positioning (not a feature matrix)

- Team -- Why this team will win

- Financials -- Revenue trajectory, burn rate, key assumptions

- The ask -- How much you are raising, what you will do with it, key milestones

Do not:

- Use more than 20 slides

- Put walls of text on any slide

- Hide bad metrics (investors will find them)

- Use unrealistic financial projections

Do:

- Lead with your strongest metric

- Tell a story, not just present data

- Make every slide pass the "so what?" test

- Practice until you can deliver it in 15 minutes flat

Step 4: Write Your Investor Update / Memo

Some investors prefer a written memo over a deck, especially at Series A and beyond. Even if you lead with a deck, having a 2-3 page memo ready gives you an edge.

Your memo should cover:

- What you have built and why it matters

- Your traction to date (be specific with numbers)

- What you have learned about your market

- How you will use the capital

- Why now is the right time to invest

For a template and examples, check out our investor update email template.

Step 5: Build Your Target Investor List (100+ Names)

This is where most founders under-invest. You need a list of at least 100 potential investors, tiered by fit:

Tier 1 (20-30 investors): Perfect stage, sector, and check size fit. These are your dream partners. Research them deeply -- read their blog posts, listen to their podcast appearances, understand their thesis.

Tier 2 (30-40 investors): Good fit but not perfect. Maybe they are exploring your sector or typically invest one stage earlier/later.

Tier 3 (30-40 investors): Possible fit. Worth a conversation but lower probability.

Where to find investors:

- Crunchbase and PitchBook for fund and deal data

- Twitter/X and LinkedIn for active investors in your space

- Your existing investors and advisors (ask for introductions)

- Founder communities (YC alumni, On Deck, etc.)

- Conference speaker lists and panel participants

Step 6: Get Warm Introductions

Cold emails to investors have a response rate of about 2-5%. Warm introductions convert at 30-50%. The math is clear.

Best sources for warm intros:

- Your existing investors (they should be your biggest advocates)

- Fellow founders who have raised from your target investors

- Advisors and board members

- Lawyers and accountants who work with startups

- Accelerator networks

How to ask for an intro:

- Send the person a "forwardable email" -- a short, compelling summary they can forward directly to the investor without rewriting anything

- Make it easy: include your one-liner, key metric, and a link to your deck

- Always ask "Is this person a good fit?" before asking for the introduction

Step 7: Run a Structured Process

The biggest mistake founders make is taking meetings one at a time, as they come. This destroys your leverage. Instead, run a structured process:

Week 1-2: Warm-up. Take meetings with Tier 2 and Tier 3 investors first. Use these as practice. Refine your pitch based on the questions you get.

Week 3-4: Tier 1 meetings. Schedule your best investors in the same 2-week window. You want them all moving through their process at roughly the same time.

Week 5-6: Follow-ups and partner meetings. If things are going well, you will start getting invited to partner meetings and receiving requests for data room access.

Week 7-8: Term sheets and negotiation. With multiple investors at the same stage, you create natural urgency without having to manufacture it.

Key principles:

- Batch your meetings. Take 8-10 per week during active fundraising.

- Update all investors simultaneously. When you share a new metric or milestone, share it with everyone.

- Create a CRM or spreadsheet to track every interaction, follow-up, and next step.

- Set a soft deadline for decisions. "We are planning to close by [date]" is a reasonable thing to say.

Step 8: Navigate Term Sheets

When a term sheet arrives, do not sign it immediately -- even if you are thrilled. Here is what to focus on:

Economics:

- Valuation (pre-money): This determines your dilution. Compare to market data for your stage.

- Option pool: Investors often want a new option pool carved out before their investment, which effectively lowers your pre-money valuation. Negotiate the size carefully.

- Liquidation preferences: 1x non-participating is standard and founder-friendly. Anything more aggressive (2x, participating preferred) deserves scrutiny.

Control:

- Board composition: Who gets board seats? Maintain founder control as long as possible.

- Protective provisions: What decisions require investor approval? These are standard but read every one.

- Pro-rata rights: Standard, and generally fine. These give investors the right to maintain their ownership in future rounds.

Other terms:

- Anti-dilution: Weighted average is standard and fair. Full ratchet is aggressive -- push back on this.

- Drag-along rights: Standard, but understand the threshold at which they trigger.

- Information rights: Reasonable reporting requirements are fine. Onerous ones are a red flag.

Get a lawyer who specializes in venture financing. This is not the time for your uncle who does real estate law.

Step 9: Due Diligence

Once you sign a term sheet, the investor's due diligence process begins in earnest. This is where your data room pays for itself.

What to expect:

- Deep dive into financial statements and projections

- Customer reference calls (investors will want to talk to 3-5 customers)

- Technical diligence (code review, architecture assessment, security audit)

- Legal review of all contracts, IP assignments, and corporate documents

- Background checks on founders

How to prepare:

- Have your data room fully organized before term sheet stage (see Step 2)

- Brief your reference customers in advance

- Prepare a technical architecture document

- Ensure all corporate documents are current and properly filed

- Address any known issues proactively -- do not let investors discover problems

A comprehensive investor data room dramatically accelerates this stage. Founders who use AppDeck's investor data room typically complete due diligence 40% faster because everything is organized, searchable, and access-controlled in one place.

For a detailed breakdown of what investors will request, see our due diligence checklist and virtual data room guide.

Step 10: Close and Announce

Once diligence is complete and legal docs are finalized:

- Wire the money. Do not celebrate until the funds are in your bank account. Deals fall apart at the last minute more often than you would think.

- Update your cap table. Make sure your cap table management tool reflects the new round.

- Inform all parties. Let the investors who did not participate know. Be gracious -- you may want to work with them in the future.

- Announce strategically. Coordinate with your lead investor on the announcement. Use it to recruit talent, attract customers, and build credibility.

- Send an investor update. Within 30 days of closing, send your first formal investor update to your new cap table. Set the cadence (monthly or quarterly) and stick to it.

Building Your Investor Data Room

Your data room is worth its own section because it is that important. A disorganized data room is the number one reason deals stall during diligence. I have seen $20M rounds delayed by weeks because a founder could not find their IP assignment agreements.

Recommended Structure

Tier 1 -- Shared at First Meeting:

- Pitch deck

- Executive summary (1-2 pages)

- High-level metrics dashboard

Tier 2 -- Shared After Initial Interest:

- Detailed financial model

- Customer case studies

- Product roadmap

- Team bios

Tier 3 -- Shared After Term Sheet (Full Diligence):

- Complete financial statements (audited if available)

- All legal documents

- Customer contracts

- Employment agreements

- IP documentation

- Tax returns

- Insurance policies

Security and Access Control

Your data room should give you granular control over who sees what and when. This is not just about security -- it is about strategy. You do not want a competitor-backed VC seeing your full customer list during a first meeting.

Key capabilities to look for:

- Folder-level permissions so you can reveal documents progressively

- Watermarking to discourage unauthorized sharing

- View tracking so you know which investors are actually reviewing materials

- Download controls to prevent bulk downloads of sensitive documents

- Expiring access to revoke permissions after a round closes

AppDeck's investor data room software was built specifically for this use case. It gives you all of these capabilities in a clean, professional interface that makes a strong first impression.

For a deeper dive, read the full investor data room best practices guide.

Fundraising Metrics Investors Care About by Stage

One of the most common questions I get from founders is "What metrics should I have before raising?" Here is a benchmark table based on hundreds of successful rounds:

| Metric | Pre-Seed | Seed | Series A | Series B | Series C |

|---|---|---|---|---|---|

| ARR | Pre-revenue | $100K - $500K | $1M - $5M | $5M - $20M | $20M - $50M+ |

| MoM Growth | N/A | 15-20% | 10-15% | 8-12% | 5-10% |

| Net Revenue Retention | N/A | 90-100% | 100-120% | 110-130% | 115-140% |

| Gross Margin | N/A | 50-70% | 60-75% | 65-80% | 70-85% |

| Burn Multiple | N/A | Under 3x | Under 2x | Under 1.5x | Under 1.2x |

| LTV/CAC | N/A | Early signal | 3:1+ | 4:1+ | 5:1+ |

| Logo Churn (Annual) | N/A | Under 5% monthly | Under 3% monthly | Under 2% monthly | Under 1.5% monthly |

| Team Size | 2-5 | 5-15 | 15-50 | 50-150 | 150-500 |

A note on these benchmarks: These are ranges from successful rounds, not hard cutoffs. If your ARR is slightly below the range but your growth rate is exceptional, you can still raise. The narrative matters as much as the numbers.

Common Fundraising Mistakes

After watching hundreds of fundraises up close, these are the seven mistakes I see most often:

1. Starting Too Late

If you have three months of runway and no term sheet, you are already in trouble. Start fundraising when you have 9-12 months of runway. The process always takes longer than you expect.

2. Not Running a Structured Process

Taking investor meetings one at a time, as they come in, is the fastest way to lose leverage. Batch your meetings. Create parallel tracks. When multiple investors are competing for a deal, terms improve and timelines compress.

3. Targeting the Wrong Investors

Pitching a growth-stage fund on your pre-seed round is a waste of everyone's time. Research every investor before you reach out. Confirm they invest at your stage, in your sector, and at your check size.

4. Under-Investing in the Data Room

Founders who treat the data room as an afterthought pay for it during diligence. Disorganized documents, missing files, and inconsistent data all erode investor confidence. Treat your data room like a product launch -- it represents the quality of your thinking and operations.

5. Ignoring Valuation Reality

Every founder thinks their company is worth more than the market says. That is natural. But insisting on an unrealistic valuation will extend your fundraise by months or kill it entirely. Benchmark your valuation against comparable recent deals and be willing to negotiate.

6. Negotiating Alone

Fundraising is a legal and financial transaction. You need experienced counsel -- a lawyer who has done dozens of venture deals and can spot problematic terms. The cost of a good startup lawyer is trivial compared to the cost of signing bad terms.

7. Going Dark After Closing

Your relationship with investors does not end at wire transfer. The founders who build the strongest investor relationships send regular updates, ask for help proactively, and are transparent about both wins and challenges. Your Series A investors are your best advocates for Series B introductions.

Frequently Asked Questions

What is startup fundraising and what are the typical stages?

Startup fundraising is the process of raising equity or convertible debt capital from angel investors, venture capital firms, and strategic investors to fund a company's growth. The typical stages are pre-seed ($250K-1M, usually angels and friends/family at the idea or early prototype stage), seed ($1M-4M for product-market fit), Series A ($5M-15M for scaling a proven model), Series B ($15M-50M for accelerating growth), and later stages (C, D, growth) for category leadership. Each stage has distinct expectations for traction, metrics, and team — raising at the wrong stage signals to investors that you don't understand the market.

How is fundraising at seed different from Series A?

Seed investors fund vision and team — you may not have revenue yet, and they're betting on your ability to find product-market fit. They expect founder-led storytelling, a credible plan, and signs of early customer pull. Series A investors fund metrics — they want to see $1M-3M ARR, repeatable customer acquisition, retention proof points, and a clear path to $10M ARR. The pitch shifts from "this could be huge" to "this is working and we know how to scale it." Founders who try to raise Series A with seed-stage traction (or vice versa) end up with month-long processes that go nowhere.

How long does a typical startup fundraise take?

A disciplined seed round takes 3-4 months from kickoff to wire transfer. Series A takes 4-6 months. Drag-out processes that stretch to 9-12 months usually indicate weak traction, an off-target investor list, or a founder running it as a side project instead of a sprint. To compress timeline: build your data room before launching the raise, line up 80-100 target investors in advance, run all pitches in parallel within a 4-6 week window to create natural urgency, and have legal counsel pre-engaged to move quickly on term sheets. Time spent fundraising is time not spent building, so the goal is a clean fast process, not a maximized round.

Who should raise venture capital vs. bootstrap or take debt?

Raise VC if you're building a software or technology company with a credible path to $100M+ in annual revenue within 7-10 years, and you need capital ahead of revenue to win a winner-take-most market. Bootstrap if you're building a profitable services or software business that can grow to $5M-30M without external capital — you keep equity, control, and optionality. Take debt (revenue-based financing, venture debt) if you have predictable recurring revenue and want to extend runway without dilution. The wrong choice — VC for a lifestyle business, bootstrap for a winner-take-most race — usually ends badly. Match the financing instrument to the business model and growth trajectory.

When should we stop a fundraise and pivot to bootstrapping or down-round?

If you've pitched 40+ qualified investors over 3 months and have no term sheets, stop the active raise and diagnose the problem honestly — traction gap, valuation expectation, market timing, or team gap. Don't keep pitching the same story to more investors hoping for a different outcome. Options at that point: take a bridge round from existing investors at the previous valuation, take a down round if survival depends on it (better than running out of cash), cut burn to extend runway 12+ months and rebuild traction before re-raising, or pivot to a profit-focused model and grow from revenue. Continuing to pitch a dead round burns founder credibility and team morale.

Conclusion

Fundraising for startups is a skill, not a talent. The founders who raise capital efficiently are not necessarily the most charismatic or the best storytellers -- they are the ones who run a disciplined process, prepare thoroughly, and respect both their own time and their investors' time.

To recap the startup fundraising strategy:

- Know your numbers cold -- what you are raising, at what valuation, and on what timeline

- Build your data room weeks before you need it

- Create a compelling deck that tells a story, not just presents data

- Build a list of 100+ investors, tiered by fit

- Get warm introductions whenever possible

- Run a structured, parallel process to create natural urgency

- Negotiate term sheets with experienced counsel

- Prepare for diligence before it starts

- Close, announce, and immediately shift into execution mode

The best fundraise is the one that gets you back to building as quickly as possible. Every week you spend fundraising is a week you are not spending on your product, your customers, and your team. Treat it like a sprint with a clear finish line, not an open-ended process.

If you are getting ready to raise and need to set up your data room, AppDeck's investor data room is purpose-built for founders running fundraising processes. It takes about 30 minutes to set up and gives you the professional foundation that serious investors expect.

Good luck out there. The fundraising game is tough, but founders who prepare well and execute with discipline consistently come out on top.

Related Reading

Founder & CEO, AppDeck

Serial entrepreneur with 20+ years building B2B software companies. Former executive managing 2,800+ employees across three continents. Vik reviews all AppDeck content for accuracy and practical relevance.

Share this article

Explore Related Solutions

Related Articles

10 AI Fundraising Tools That Actually Help Startups Raise Capital

The best AI tools for startup fundraising in 2026. Investor matching, pitch deck builders, CRM automation, due diligence prep, and outreach tools.

Due Diligence Checklist: Complete Guide for M&A, Fundraising & Investors

The definitive due diligence checklist for fundraising, M&A, and investor review. 100+ items organized by category with templates and data room setup tips.

Investor Data Room Best Practices: A CFO's Complete Guide for 2026

Learn the essential best practices for creating and managing investor data rooms. Complete guide with checklist, templates, and real-world examples from successful fundraising rounds.